⚠️ The Jefferies Crisis: What 2008 Subprime and 2025 Private Credit Have in Common

Trump and China might not be the real problem right now.

⚠️ The Jefferies Crisis: What 2008 Subprime and 2025 Private Credit Have in Common

Breaking: The CEO Wrote an Emergency Letter on a Sunday Night?!

Investment bank Jefferies saw its stock plunge roughly 18% over five days after a $715M exposure to bankrupt auto parts supplier First Brands was revealed. CEO Rich Handler and President Brian Friedman issued an emergency public letter on Sunday night: “The losses are absorbable. The market reaction is excessive.”

Unwritten Wall Street rule: When a CEO writes an emergency letter on a weekend, it’s a signal that the crisis is real.

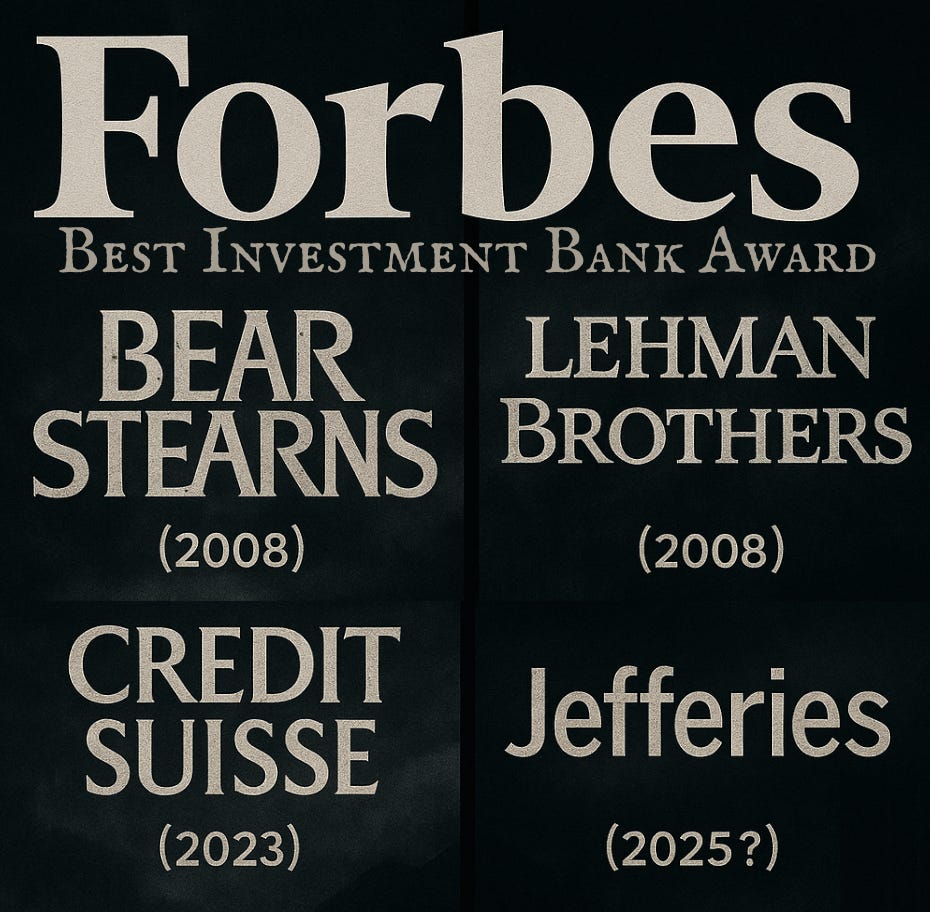

History proves it:

Bear Stearns (2008): “We’re fine” → Bankrupt 2 weeks later.

Lehman Brothers (2008): “Liquidity is sufficient” → Bankrupt 1 month later.

Credit Suisse (2023): “Greensill is a small issue” → Fire-sale acquisition 2 years later.

Jefferies stock is down ~18%. Whether this is an “overreaction” or not — we’ll find out soon enough.

What Happened?

The $715M Black Hole

Jefferies’ subsidiary trade finance hedge fund Point Bonita Capital was exposed to $715M in bankrupt auto parts supplier First Brands. That’s nearly 25% of Point Bonita’s $3B portfolio.

Here’s the structure: Point Bonita purchased invoices that First Brands had issued to retailers like Walmart, AutoZone, and NAPA for products like wipers and oil filters (invoice factoring).

But there was a fatal design flaw:

In theory: Walmart → pays Point Bonita directly. In reality: Walmart → pays First Brands (as “Servicer”) → First Brands forwards to Point Bonita.

First Brands acted as “Servicer,” receiving Walmart’s payments and supposedly passing them through to Point Bonita. In other words, Point Bonita gave First Brands money, and First Brands was supposed to give it back. The fund may never have received a single dollar directly from Walmart. Its lifeline was entirely in the hands of the very borrower it was supposed to be protected from.

On September 15th, that lifeline snapped. First Brands suddenly stopped forwarding retailer payments to Point Bonita. Money that had flowed without a single missed payment for six years — gone overnight.

Double Factoring Allegations: $2.3B Vanished Into Thin Air

A First Brands special investigation team is currently examining the possibility that the same invoices were sold to multiple parties simultaneously (double factoring).

An emergency filing by Raistone’s attorneys is even more shocking:

“According to sworn statements by the debtor’s representative and counsel, up to $2.3B in third-party factoring financing has simply vanished.”

When Raistone’s law firm Orrick asked First Brands’ law firm Weil “where did that enormous amount of money go, and how much is currently recoverable?” — the response was:

“We don’t know... $0.”

The infamous Weil email explained We have all seen the below image, but what do it mean? In an October 2 exchange between Weil and Orrick, Weil acknowledged")

The same Walmart invoices were allegedly sold to Jefferies, then to another fund, then to yet another. This is rehypothecation fraud. And on Wall Street, 70% of companies that say “we’ve never done that”... well, you know how that story ends.

DOJ Investigation

Per FT reporting, the U.S. Department of Justice has launched an investigation. This isn’t just a civil bankruptcy — they’re looking at potential criminal fraud.

Who Is Jefferies?

Jefferies Financial Group — not a bulge bracket like Goldman Sachs or Morgan Stanley, but not small either. A mid-tier investment bank with $10.5B in total assets, $8.5B in tangible equity, and $11.5B in cash on the books.

Jefferies had been First Brands’ primary bank for over a decade, present throughout its growth from a small parts company to a major auto components player. The criticism now: the bank got too close to the client and let risk management slip.

Recently, Jefferies expanded its strategic alliance with SMBC (Sumitomo Mitsui), which had planned to increase its stake from 14.5% to 20%. That increase is almost certainly on hold now. The key question is how much damage SMBC absorbs.

A Wall Street Bank Run Has Begun

Institutions Heading for the Exits

As of October 11th, confirmed redemption requests:

BlackRock (world’s largest asset manager) — first redemption request filed.

Texas Treasury Safekeeping Trust — early redemption.

Morgan Stanley — formally initiated redemption procedures on October 11th.

This is a textbook Wall Street bank run.

Damage Spreading: Who Else Got Hit?

Direct exposure: UBS funds: First Brands-related risk represents 30% of assets. Cantor Fitzgerald: renegotiating its UBS O’Connor acquisition deal because of this. Western Alliance: passively entangled via leverage financing provided to Jefferies. Raistone: $631M exposed, half of staff laid off.

Across the Pacific: Norinchukin Bank + Mitsui & Co. joint venture: potential losses up to $1.75B. Allianz and other insurers: preparing for major claims.

How does one auto parts company’s bankruptcy entangle global financial institutions? This is the truth that trade finance’s “it’s safe” mythology has been hiding.

Why Now: “It Smells Like Subprime”

Jim Chanos’s Warning

Jim Chanos — the legendary short seller who called Enron in 2001 — recently warned:

“The current booming private credit market is operating in ways similar to the subprime mortgages that triggered the 2008 global financial crisis.”

What Chanos sees in common between 2008 Subprime and 2025 Private Credit:

Black box structures: Multi-layered structures that hide risk.

Excessive yields: First Brands collateral inventory debt was expected to yield over 50%.

Opacity: Enron at least had public disclosure obligations as a listed company. First Brands is a private company — only hundreds of loan managers with confidentiality agreements could access its financials.

“We rarely get to see how the sausage is made.” — Chanos

This isn’t a simple corporate bankruptcy. It’s the private credit market’s mask coming off — the market everyone thought was easy money, safe money, money-on-money. And the market is in an uproar because this echoes the Greensill Capital and Archegos events that brought down Credit Suisse.

Greensill Capital (2021): $10B Evaporated

Structure: UK fintech Greensill grew rapidly in trade finance post-2008. Companies sell products to big retailers, get invoices, and Greensill buys those invoices at a discount for instant cash. “Safe” — because Walmart is guaranteeing payment, right?

Problem: Same invoices repackaged and sold multiple times. They started selling future invoices that didn’t even exist yet. Credit Suisse had $10B+ invested in Greensill. 2021: Greensill goes bankrupt → Credit Suisse takes $10B loss.

Archegos Capital (2021): $5.5B in Losses

Structure: Bill Hwang’s family office took massive leverage from multiple banks — none of which knew how much the others had lent. Total return swaps hid actual positions. Reality: $200B+ in positions on $10B in capital (20x leverage).

Problem: March 2021, several stocks crash, margin calls hit, Hwang can’t pay → banks panic-sell. Credit Suisse: $5.5B loss. Nomura: $2.9B loss.

Credit Suisse endgame: Greensill ($10B) + Archegos ($5.5B) = total trust collapse → 2023 fire-sale to UBS.

Why First Brands Is Greensill + Archegos 2.0

The terrifying commonalities: multi-layered opaque structures, duplicate collateral sales, hidden leverage, excessive yields masking risk, and cascading counterparty exposure.

The difference? First Brands carries the DNA of both events:

Like Greensill: trade finance + selling the same collateral to multiple buyers.

Like Archegos: opaque structure + hidden debt.

Worst-Case Scenario: Financial Market Seizure

Double factoring confirmed → same invoices sold to 5 funds.

Jefferies criminal indictment + side letter lawsuit explosion.

Stock -60% → Point Bonita redemption cascade.

Forced liquidation → larger losses → trust collapse spreads across Jefferies’ entire $20B+ in managed funds.

UBS, Millennium found to have similar black boxes.

Entire $1.7T private credit market freezes.

LPs demand full redemptions → fund fire sales.

Leveraged loans crash -30% → Raistone, Onset, and other supply chain financiers fail in sequence.

Small and mid-size businesses lose access to working capital → supply chain paralysis.

Jefferies attempts a Credit Suisse-style sale but finds no buyer → bankruptcy → $10B in equity evaporates.

2008 Subprime = one mortgage repackaged into multiple CDOs. 2025 First Brands = one invoice sold to multiple funds.

Same shit, different wrapper.

So What?

Private Credit’s Winter Is Coming. The “Safe Investment” Fantasy Is Collapsing.

Everyone thought: “It’s an invoice guaranteed by Walmart. Default risk is basically zero, right?”

But it turns out the same invoice may have been sold to Fund A, Fund B, and Fund C simultaneously. Walmart pays $1M, but three funds each claim $1M. Who gets paid? Whichever one races to bankruptcy court first.

Point Bonita was registered in the bankruptcy filing as an unsecured creditor with a “contingent, unliquidated, disputed claim.” Translation: “We have no idea if we’re getting our money back.”

This is the real problem with the private credit market. What everyone believed was “safe” was actually a collection of hidden leverage and duplicate collateral.

In 2008, everyone said “subprime is a small problem.” Until Lehman blew up.

If trade finance — supposedly the safest corner of private credit — can blow up like this, what about the rest?

Inside this massive black box that attracted everyone with high yields — how many more time bombs are hiding?

If First Brands is the trigger, we might be witnessing another moment that goes down in financial history.

Thanks for reading, as always.

— Ian